With economic uncertainty building, many business owners are questioning whether their operations could survive a downturn. To gauge how prepared they are, we surveyed 600 owners across industries. The results reveal major weaknesses in cash flow, access to financing, and confidence in long-term survival, especially if revenue slows or stops. Strengthening these areas with planning and flexible funding could be key to staying resilient in tough times.

Key Takeaways

-

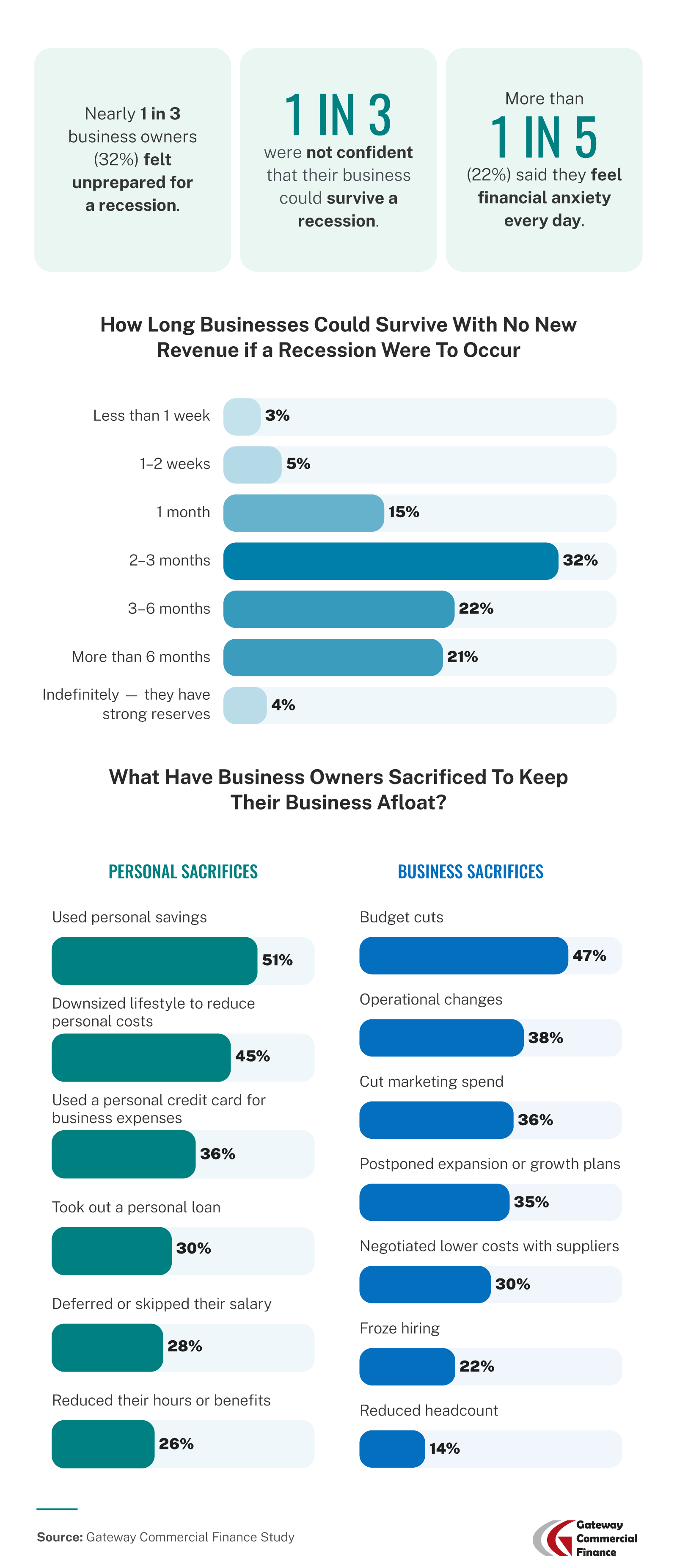

- 32% of business owners feel unprepared for a potential recession, and 1 in 3 are not confident their business would survive if one were to occur this year.

- In a recession, about 1 in 4 business owners predict they could only survive a month or less with no new revenue.

- 22% of business owners experience financial anxiety daily.

- 47% are making business budget cuts, and 51% have used personal savings to keep their business afloat.

- More than 1 in 3 business owners (36%) are not confident they can secure a business loan this year.

Financial Strain and Recession Concerns Among Business Owners

Recession preparedness is uneven among business owners, and for many, the outlook is worrying. Financial anxiety and short survival windows point to serious vulnerabilities.

A third of business owners said they aren’t confident their company would survive an economic downturn if one were to happen. Even more concerning, 22% reported feeling anxious daily about finances and the health of their operations.

Some businesses also lack preparedness. Nearly a third (32%) admitted they feel unprepared to handle the results of a recession this year, and more than 1 in 10 (11%) said they are not at all “recession ready.”

Survival timelines in the face of halted revenue reveal a pressing vulnerability. Just 4% of business owners say they could survive indefinitely without new income due to their strong reserves. A much larger group—32%—said they’d only last two to three months under such conditions, while 23% could last just a month or less.

To manage ongoing expenses and stay afloat, many business owners have made significant personal sacrifices. More than half (51%) used their own savings, while 30% took out personal loans to support their business during tight periods. As for business sacrifices, the top cuts made were to budgets (47%), operations (38%), and marketing (36%).

The Toll of Late Client Payments on Businesses

Cash flow disruptions caused by slow-paying clients continue to threaten business operations. Many owners are forced to delay payments, miss payroll, or take on additional risk.

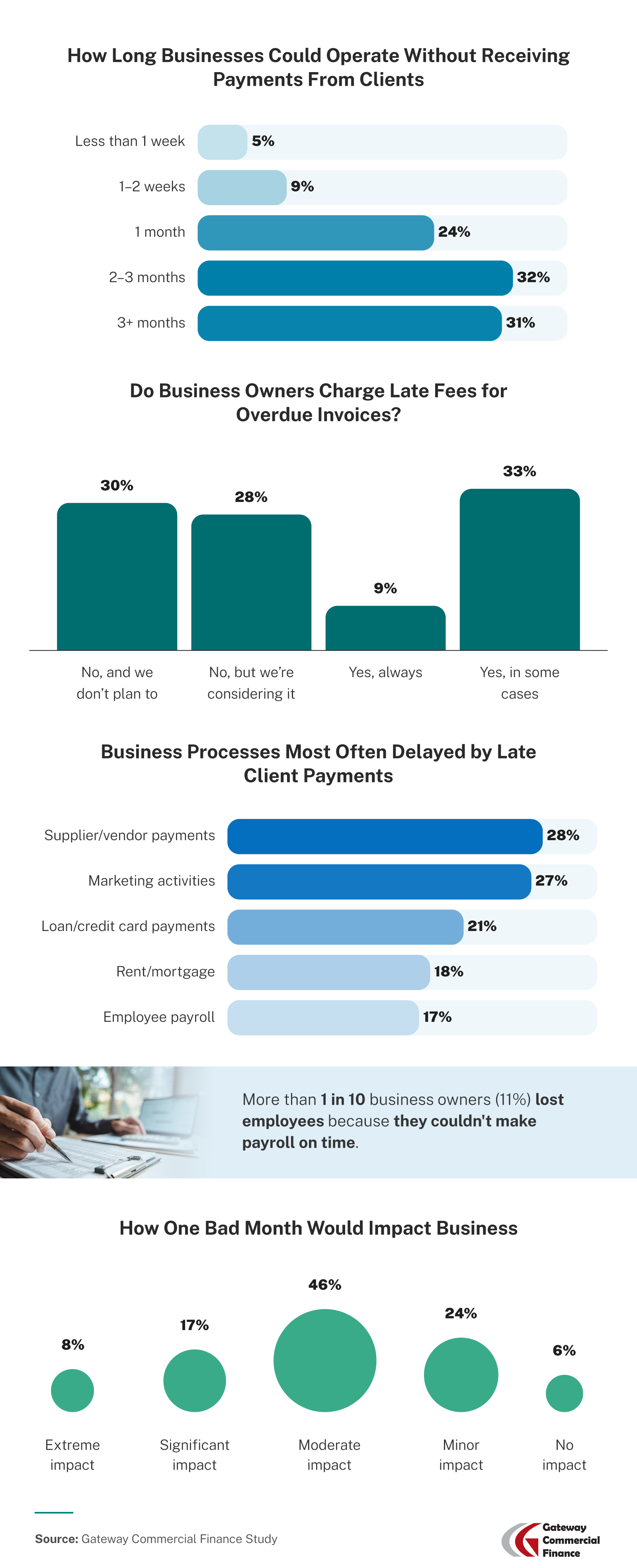

Late client payments are common and damaging for businesses. Two-thirds of business owners (66%) reported experiencing missed or delayed payments in the past year, yet only 9% always charge late fees. A third said they only charge them occasionally.

The impact of these delays can be serious. While 61% believed they could operate for more than two months without incoming payments, 24% could only last a month, and 14% couldn’t survive beyond two weeks. Payroll is often one of the first areas to be affected. Seventeen percent of owners said they’ve delayed payroll due to late client payments, and 11% reported losing employees after struggling to meet payroll deadlines.

These payment gaps ripple through other areas as well. Over 1 in 4 (28%) have had to delay payments to suppliers, and many have also postponed paying for marketing, loans, and rent.

Financing Frustrations and the Rise of Alternative Funding

With many business owners struggling to access traditional financing, alternative funding options are gaining traction as a potential safety net.

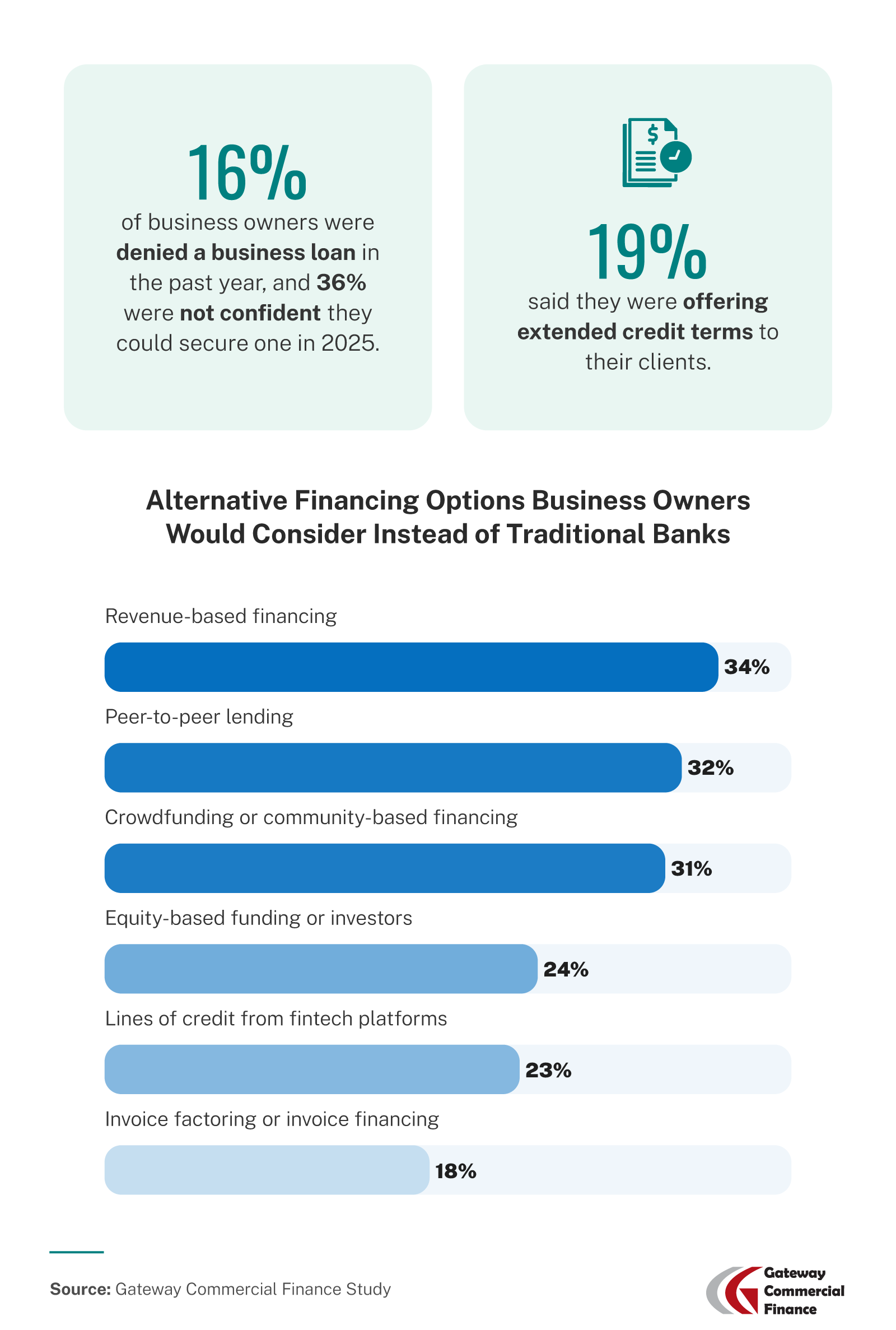

Securing capital has proven difficult for many. Sixteen percent of business owners were denied a loan in the past year, and 36% were not confident they would be able to get one this year. To maintain customer relationships and bring in sales, 19% of business owners said they are offering extended credit terms to clients, though this approach could strain their own cash reserves.

A number of businesses are open to alternative forms of funding. In place of a traditional bank, 34% said they would consider revenue-based financing, while 32% are willing to try peer-to-peer lending. Another 31% were looking to crowdfunding or community capital as funding sources.

Nearly 1 in 5 business owners (18%) said they would consider invoice factoring. This financing method allows businesses to turn unpaid invoices into immediate working capital without taking on new debt. Instead of waiting 30 to 90 days for customer payments, a company submits its outstanding invoices to a factoring provider, who then advances a large portion of the invoice value, usually within 24 hours.

Once the client pays the invoice, the factor deducts its fees and the advance amount and then releases the remaining balance. For businesses under cash flow pressure, especially those offering extended terms to customers, factoring can provide the liquidity needed to cover payroll, restock inventory, or take on new work.

Conclusion: Final Thoughts on Recession Readiness

Recession fears are valid, and the numbers show many businesses are not as financially prepared as they’d like to be. From high anxiety levels and reliance on personal funds to the cash flow pinch caused by late payments and uncertain financing access, the path forward requires both caution and adaptability. For businesses feeling the strain, alternative funding solutions may offer the breathing room needed to stay strong during economic turbulence.

Methodology

We surveyed 600 business owners on June 9, 2025, to assess their financial readiness for a potential recession. All responses were self-reported. Percentages may not total 100% due to rounding.

About Gateway Commercial Finance

Gateway Commercial Finance provides fast, flexible working capital solutions for B2B companies facing cash flow gaps. Whether you’re managing slow-paying clients or preparing for uncertain economic conditions, Gateway helps you unlock the value of your receivables with reliable invoice factoring services tailored to your business needs.

Fair Use Statement

If you’d like to share these findings, you’re welcome to do so for noncommercial purposes. Please include a link back to Gateway Commercial Finance for proper attribution.